Superannuation cap to rise: what it means for your retirement

And in today's newspapers, 'Retirees reap the rewards after another year of sky-high super returns'

In this edition

Feature: Superannuation cap to rise: what it means for your retirement

Course: Kicks off on the 13th Feb

From Bec’s Desk: Back in the hot seat

SMH/TheAge: Retirees reap the rewards after another year of sky-high super returns

Prime Time: Knowing when to retire

Now for a message from our terrific sponsors… Viking.

Enjoy Free Flight Offers on 2025-2027 Voyages with Viking’s Explorer Sale

Sail with Viking to extraordinary shores and for a limited time, enjoy free flight offers with your booking.

Whether by river or ocean, Viking has crafted unforgettable journeys across all seven continents so you can explore more of the world. With 150 unique itineraries ranging from 8 to 170 days in duration, discover immersive experiences and cultural enrichment in every destination you visit.

Book your 2025-2027 cruise by 31 March 2025 and enjoy free flight offers with Viking’s river, ocean or expedition voyages, valued up to AU$2,400 per person.* Plus receive AU$500 shipboard credit with any ocean and expedition booking. (*T&C’s apply)

Super cap to rise: what it means for your retirement

The latest CPI figures landed this week, confirming that from 1 July 2025, the transfer balance cap (TBC) will increase from $1.9 million to $2 million. This means Australians can shift more of their super into the tax-free retirement phase.

Super contribution caps are tied to a different benchmark (AWOTE), which hasn’t increased enough to trigger a change. So for now, the limits on Non-Concessional Contributions (NCC) and Concessional Contributions (CC) are staying the same.

If you’re already in retirement phase or approaching it, this increase could give you a better opportunity to maximise tax-free super earnings. The transfer balance cap sets the limit on how much you can transfer into a retirement-phase pension account, where earnings are not subject to tax. Any amount over this cap remains in an accumulation account, where earnings are taxed at 15%.

The increase is triggered by the latest CPI figures released this week, confirming that indexation targets have been met, pushing the cap up to $2 million from July 2025.

How does this affect someone planning for retirement?

If you haven’t yet started a retirement-phase pension and you have in excess of $1.9M to consider, the new $2 million cap applies in full after it kicks in in July 2025. If you’ve already used part of your cap, your remaining cap will increase in proportion to the unused amount. For example, if you haven’t yet moved any super into retirement phase, you can now transfer up to $2 million tax-free from July 2025. If you’ve previously used $1.4 million of your cap, your personal cap will increase proportionally, meaning you’ll have more room to transfer additional super into the tax-free phase.

With more of your super eligible for the tax-free retirement phase, your investment earnings won’t be subject to the 15% accumulation tax, helping to stretch your retirement savings further. This is particularly beneficial in a rising market, where compounding tax-free returns can significantly boost long-term income.

What should you do?

For those nearing retirement, now is the time to review your super strategy to make the most of the increased cap – if you are someone with close to $2M in super to manage. Checking your super balance to see how much you can transfer, reviewing your fund’s performance to ensure it aligns with your income needs, and speaking to a financial adviser to optimise your transition to retirement phase are all key steps.

While the increase happens automatically, a little planning can help you make the most of the higher limit. If your balance is just over the $1.9 million cap, you might consider keeping contributions in accumulation mode until the change kicks in. Not many will be at this level, but it’s still useful to know. As always, chat with an adviser for personalised advice on how this fits into your strategy.

It’s been a bit of a whirlwind week—half spent freezing in Canada on the most wonderful family break, then flying home, only to be hit with Queensland’s intense heat. In between sweating it out, I’ve been deep in prep mode—getting the course ready, writing newsletters, and pulling together fresh articles. Now that the year is kicking into gear, I can’t wait to share what’s ahead… but for now, you’ll have to watch this space.

I’m well and truly back at my desk, signing books and packing welcome packs like a demon for our biggest-ever cohort of the How to Have an Epic Retirement Flagship Course—hundreds and hundreds are already in! If you haven’t locked in your spot yet and missed the early bird deal, don’t panic—you can still use LASTMINUTE15 for 15% off the full-priced program. But don’t wait too long—I need time to get your welcome pack in the mail! The course kicks off on the 13th February - and runs for six weeks. There’s more information on our website here.

This week’s podcast was an absolute delight to record! If you're thinking about retiring, you won’t want to miss my conversation with Terri Bradford. She brings a fantastic mix of personal experience and professional insight—it’s a must-listen. Be sure to tune in!

Last week, so many of you jumped into the comments on the newsletter, and I was thrilled to see such lively discussions around the topics raised. Now, we’re taking it a step further—some of your questions will be answered in an upcoming podcast! So, keep the comments and questions coming—your input helps me help you.

Lastly, I’m loving getting your questions, ideas and letters. I love hearing from you and being guided by you on what really matters as you approach retirement. Please, send your letters to me simply by pressing reply to this email.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Retirees reap the rewards after another year of sky-high super returns

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 26th January 2025.

The official data is in, and 2024 was a ripper of a year for super. But the real winners? Retirees in pension-phase funds, who locked in even better returns than their accumulation-phase counterparts.

That’s not surprising – tax-free earnings give them a natural edge. But what’s worth paying attention to is just how much better some funds performed.

This raises a key question: Are you making the most of the upside retirement phase funds are achieving? If you’re already in pension phase, is your fund delivering top-tier returns over the long and the short term?

And if you’re still in accumulation, are you planning your transition into the retirement phase wisely to maximise the benefits? The gap between an average fund and a high-performing one adds up significantly over the long term – and in retirement, every dollar counts.

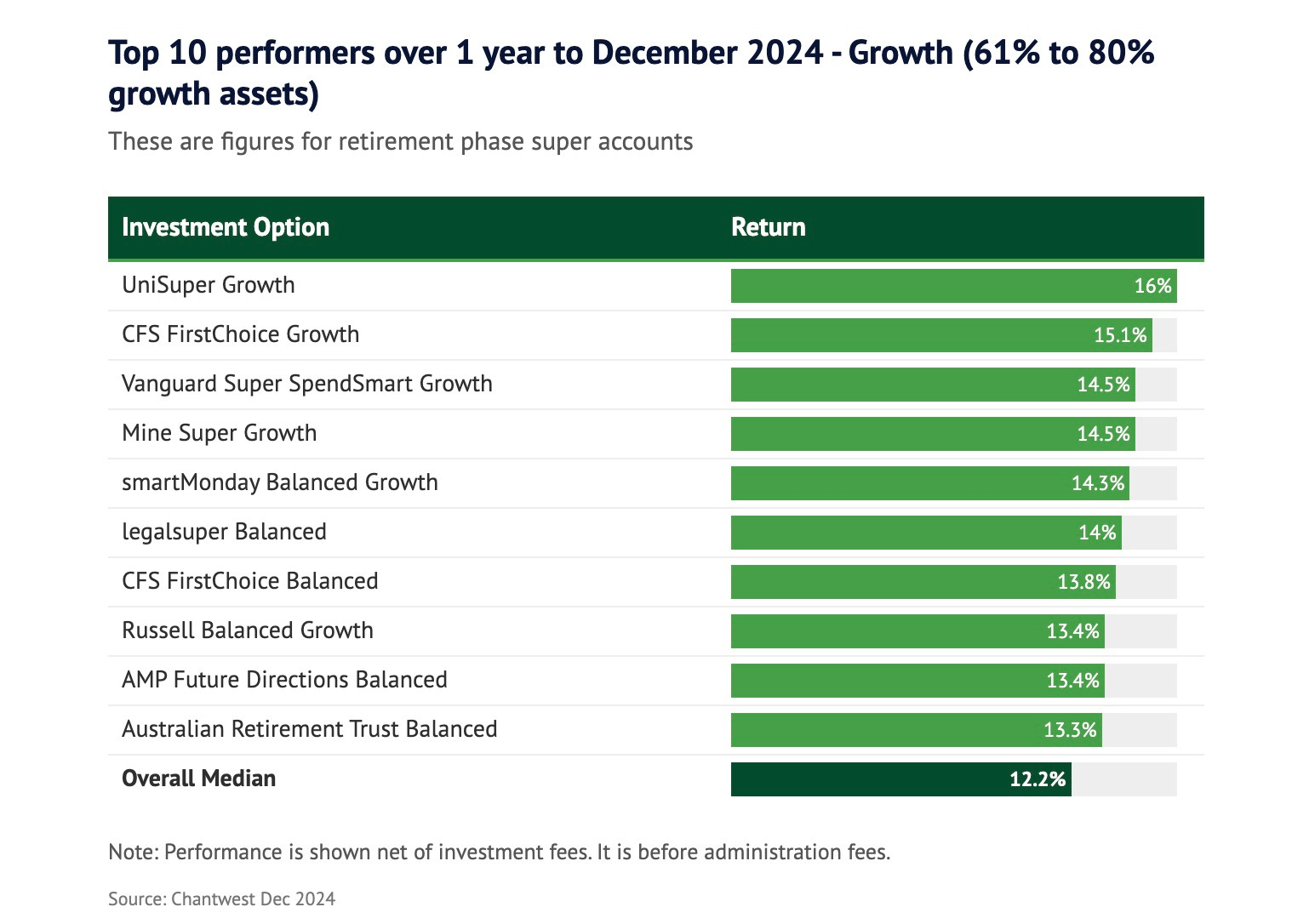

For most Aussies still in accumulation, growth funds (those with 61-80 per cent in growth assets) delivered a solid 11.4 per cent over the calendar year according to data sourced this week from Chantwest. But if you were in pension phase? Even better – an average return of 12.2 per cent.

That’s a clear win over the S&P/ASX 200’s 11.2 per cent gain (dividends included). Not bad at all, especially when you remember that every cent of those pension-phase returns is tax-free.

Leading the pack in both phases was Unisuper’s Growth Fund, which returned 16 per cent in retirement phase against 14.7 per cent in accumulation, followed closely by CFS FirstChoice at 15.1 per cent in retirement and 13.6 per cent in accumulation; and Mine Super with returns of 14.5 per cent in retirement phase and 13.4 per cent in accumulation.

This article continues — Read on, in The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

Knowing when to retire

Today’s episode is all about navigating one of the biggest transitions we face in midlife: knowing when and how to step back from full-time work—or even retire. I’m joined by the inspiring Terri Bradford, former Head of Wealth Management at Morgans Financial, who spent 25 years as a leader in the finance industry. With her extensive expertise, Terri made the bold decision to transition into a flexible, part-time pre-retirement phase—what I like to call her Prime Time. And she joins us today to help everyone better understand how to know when the time is right.

Terri’s story is both relatable and a testament to her deep understanding of this space. She shares how her decision was shaped by health challenges, demanding travel schedules, and a desire to prioritise her relationships and well-being. From her unique vantage point as a financial expert, she offers us actionable insights into recognising the signs it’s time to step back, planning for financial and emotional readiness, and avoiding the pitfalls many people face when making this transition.

But Terri’s journey isn’t just about stepping back—it’s also about staying connected to meaningful work, rediscovering hobbies, and embracing reinvention. I’m quite sure her thoughtful perspective and expert advice will resonate with you — whether you’re actively planning your next phase or just starting to explore what your life might look like in five or ten years and when time might be right for you to explore the ‘R’ word. Let’s dive in!

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Last of all, if you haven’t read the book, you can order your copy from Amazon online and Big W online too. Or pick up a copy at your local Big W, or QBD stores.

Hi. If you super is in accumulation phase & you have reached pension age do you have to withdraw the minimum 5%, or is that only required in pension phase? Thanks.

if you have a current pension account can you add to it up to the available cap