Think you need $1 million+ to retire? These new benchmarks might surprise you

And in today's newspapers, 'Could mandatory annuities solve our retirement woes?'

In this edition

Feature: How much do you really need in savings to retire? New benchmarks

Course: Last call on earlybird spots

From Bec’s Desk: A quick break

SMH/TheAge: Could mandatory annuities solve our retirement woes?

Prime Time: Everything you need to know about weight loss drugs

The Autumn Flagship Course now 25% off - last weekend

Time is running out! Our 25% off Earlybird deal on the Autumn Edition of the How to Have an Epic Retirement Flagship Course ends this Sunday.

The program begins on 13th February, with kickoff packs being sent out next week. Don’t miss your chance to secure your spot at this discounted rate—book now before prices go up!

This six-week program is the only high-quality, live, and interactive retirement education experience available, designed to give you the tools, confidence, and clarity to create the retirement you deserve.

Get in now while there’s still time to save! Want to learn more or download our brochure? ➡️ visit the website here

Think you need $1 million to retire? These new benchmarks might surprise you

Some new and different benchmarks to consider.

If there’s one question that keeps pre-retirees awake at night, it’s this: How much is enough to retire? For years, we’ve been bombarded with figures like $1 million or more, making many people feel like they’re running an unwinnable race. In the book, How to Have an Epic Retirement, I explain in detail how to calculate your own number—which is the best way to go about predicting how much you need.

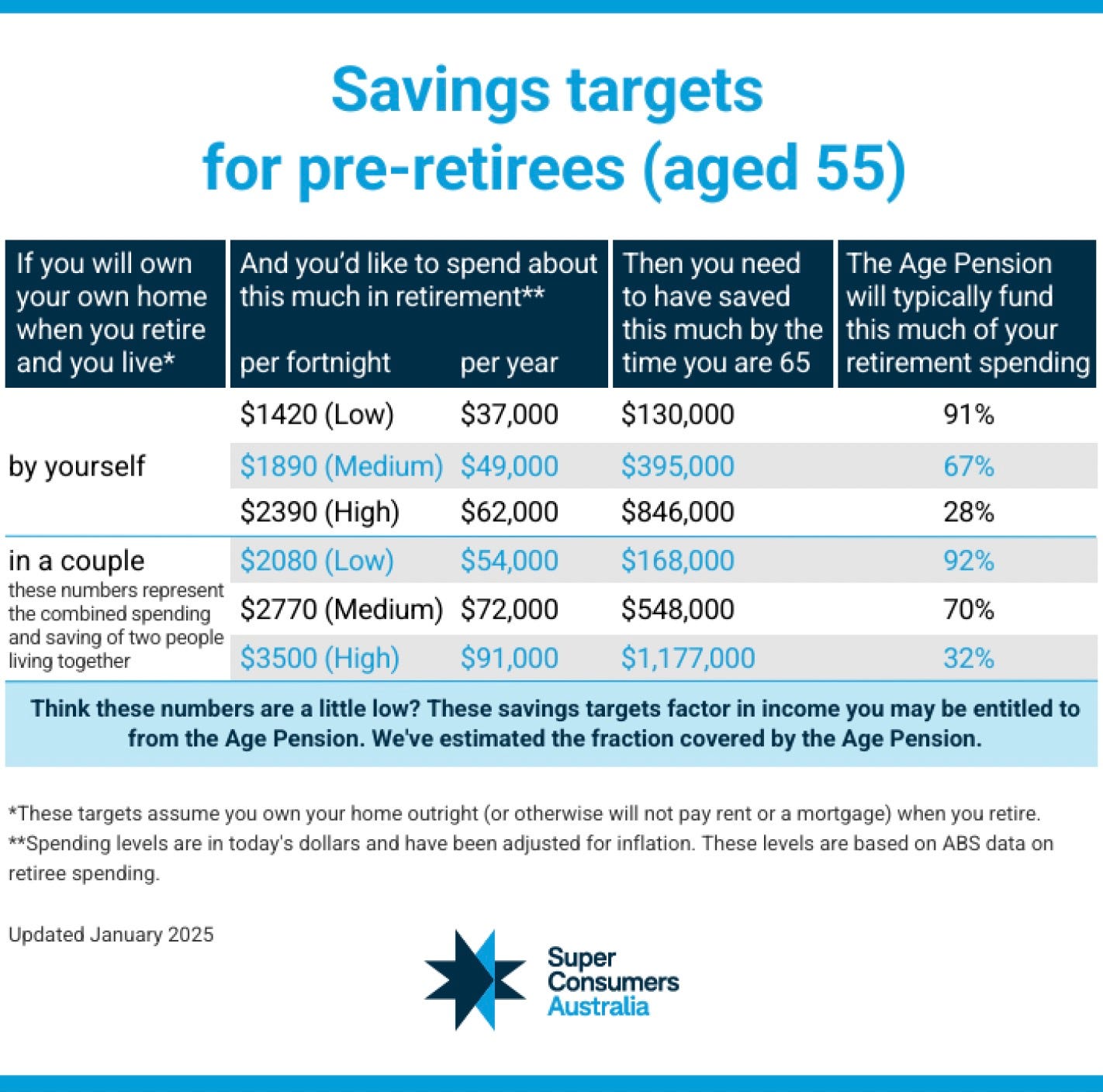

But this week, some benchmarks I don’t normally report on were released: the Super Consumers Australia benchmarks. They’ve created a really helpful table to guide people who are in pre-retirement today, both singles and couples, about how much they might need to retire based on their current fortnightly cost of living expectations. It’s a refreshingly practical way to approach retirement planning because it ties your savings target to how you actually live, instead of throwing generic figures at you and hoping for the best.

The numbers take into account the age pension and help you contemplate what portion of your retirement income will be subsidised by it over time too. Interestingly, these benchmarks come in much lower than the widely used Retirement Standard provided by the Association of Superannuation Funds of Australia (ASFA), making them a valuable tool for evaluating your planning — especially if you’re planning for retirement without ‘a lot’ of money.

Now that you’ve had a look, let’s explore some of the conclusions you might be able to draw, depending on your circumstances.

A modest lifestyle and the age pension can work if you own your own home

Let’s start with the surprising reality: if you’re planning to spend $37,000 per year in retirement (a "low" cost lifestyle in today’s dollars) and you own your home outright, you might only need $130,000 in savings according to these benchmarks. Why? Because the Age Pension could cover up to 91% of your retirement income needs in this situation. The key is to focus before retirement on owning a home you can afford. If you haven’t already taken the time to understand it, take time to learn about ‘the sweet spot’. You can read more about it here.

Retiring as a couple makes a huge difference to the cost of retirement

There’s no doubt about it: retiring as part of a couple makes a big difference to how much you can afford. Let’s say you and your partner want to spend $72,000 a year (a "medium" cost lifestyle today by these benchmarks). You’d need $548,000 in combined savings by age 65 to make it work. Compare that to a single person aiming to spend $49,000 a year, who would need $395,000. The difference between the two really highlights the power of sharing costs like utilities, groceries, and even travel expenses.

The age pension: a significant contributor to a comfortable retirement for many

One of the most interesting insights from these numbers is just how much the Age Pension is doing the heavy lifting in Australia today. For medium spenders, it’s covering 67% of a single person’s retirement needs and 70% for couples. That’s massive. And more than 62% of retirees today draw on the age pension in some form or another. So you’re expected to consider it in your planning.

What about big-spending retirements?

For those dreaming of a higher-spending lifestyle—let’s say $91,000 a year as a couple or above—the target for superannuation savings when you retire at 65 (the average age of retirement in Australia) jumps to $1.17 million or above. That’s a big number for some to contemplate saving, but it’s important to remember that it can come from multiple sources. Many retirees contemplate downsizing, tapping into investments outside super, or even working part-time during the early years of retirement to allow them to build up their superannuation nest egg to higher levels.

If these numbers raise questions — leave them for me in the comments and I’ll answer them in future newsletters.

With the new year still in its early weeks, the second edit for Prime Time (the book) underway, and the first draft of International Epic Retirement off to the publishers, I took a bit of a break — taking off for a quick visit to see my daughter in Canada before the year hits full swing. It’s been a lovely end to the Christmas and New Year holidays and a great reward for finishing my book. Hopefully - you didn’t even notice I was gone as I really can do a lot of what I do while I’m on the road.

This week will see me back on Aussie soil and firmly in the thick of 2025 with the kickoff of the How to Have an Epic Retirement Flagship Course now just two weeks away. I have books to sign and mailbags to pack — lots and lots of mailbags — an exciting prospect as we gear up for the largest Epic Course cohort ever for this program.

I’m also diving into proactive action for the year ahead — preparing speeches, programs and podcasts to make navigating pre-retirement and retirement easier. If you’re organising retirement planning events this year and are looking for a speaker/educator, do keep me in mind. I love educating people on how to have an epic retirement — whether it’s for corporate groups or individual consumers.

And finally, don’t hesitate to reach out with your questions, ideas and letters. I love hearing from you and being guided by you on what really matters as you approach retirement. Please, send your letters to bec@epicretirement.com.au.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Could mandatory annuities solve our retirement woes?

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 26th January 2025.

The Grattan Institute has dropped a report this week that’s got everyone talking. It tackles a familiar issue: Australians are nervous about spending their retirement savings.

Most retirees live off the income their super generates, leaving the capital untouched to pass on as a legacy. The problem? Many are living far below the standard they could comfortably afford, simply because they’re too cautious to dip into their savings. And the real purpose of superannuation – to fund our retirements is being neglected.

The report also points out what we’ve all been saying for years: the superannuation system is far too complex, and there’s virtually no support to help people figure out how to navigate retirement once they stop working.

The proposed solution? The Grattan Institute suggests the government step in and start offering lifetime annuities – products that already exist that are designed to provide retirees with a secure, steady income stream for life.

It even floated the idea of making these annuities mandatory, so everyone has some peace of mind in retirement and no one has to worry about running out of money.

It’s a bold suggestion, and for me, it raised some big questions about whether lifetime annuities could be the key to giving Australians the confidence to spend their super and live more comfortably. Whether it’s the shake-up we need or just another idea that will spark a lot of debate, one thing is clear: the way we think about funding our retirement needs to change.

I’m going to set aside the controversial calls of the Grattan Institute for now and instead focus on the big lessons we can take from this report. And there are three...

This article continues — Read on, in The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

Everything you need to know about weight loss drugs

Metabolism, weight loss, and the science behind midlife health with Professor Michael Cowley from Monash University.

It's that time of year again—the gyms are packed, everyone's talking about their new diet, and we’re all vowing to be our best selves in 2025. But let’s face it, for those of us in midlife, weight loss can feel like an uphill battle, no matter how many resolutions we make. So, what’s really going on with our bodies? And could the buzzworthy weight-loss drugs like Ozempic, Mounjaro and Wegovy be the game-changer they’re hyped up to be?

In this episode, I sit down with Professor Michael Cowley, a leading physiologist and weight loss expert from Monash University, to separate the myths from the facts. We dive into what actually happens to your metabolism as you age, how these drugs work, and what they’re really doing to your body. Whether you’re curious about the science, considering your options, or just want a deeper understanding of how to tackle weight gain in midlife, this conversation is a must-listen.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Last of all, if you haven’t read the book, you can order your copy from Amazon online and Big W online too. Or pick up a copy at your local Big W, or QBD stores.

Bec. The Grattan Institute’s so called suggestion that Government should make Superannuation annuities mandatory is completely outrageous. This money is the property of the individual and has already had tax paid on it. It’s up to the individual as to how and when they spend it. If they want to live a frugal lifestyle then that’s their choice. This smacks of a state controlled/ communist style system that has no place in our democratic Australia. I may add many Superannuants are self- funded retirees so again saving the taxpayers having to fund their retirement. Furthermore, if the Grattan Institute is so keen to help people spend their money then try starting with some of their own. Butt Out Grattan Institute.

Hello Bec. What amount of super do you need to live on $72 - $92K a year when you don't factor in the age pension. We have our home and a holiday home, so don't qualify for the age pension. Thanks Randall